From Backup Power to Grid Asset

Battery storage no longer waits quietly in the background. Across Australia, the industry is witnessing a decisive transition: energy storage systems (ESS) have shed their passive "backup power" identity and are stepping into the operational core of the grid — trading energy, stabilizing frequency, and coordinating distributed resources in real time. This is not a future scenario. It is already happening.

The Old Narrative No Longer Holds

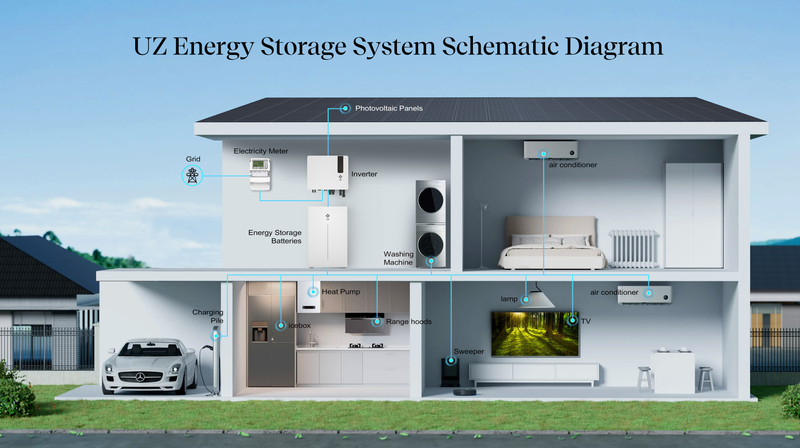

For years, the standard pitch for battery storage was straightforward: charge from solar during the day, discharge at night, keep the lights on when the grid goes down. The value was local, reactive, and largely invisible to the broader electricity system.

That narrative is now structurally obsolete.

Australia's National Electricity Market (NEM) has undergone a fundamental shape shift. According to the Australian Energy Market Operator (AEMO), renewables accounted for 46.5% of NEM generation in Q1 2026, with rooftop solar continuing to suppress daytime wholesale prices — often driving them into negative territory. By evening, as solar output collapses and demand surges, the system faces steep ramp challenges that legacy generation cannot always meet cleanly.

The grid's primary challenge is no longer generating enough electricity. It is managing the timing mismatch between when power is produced and when it is consumed.

This is the structural opening through which battery storage has moved — from peripheral resilience tool to indispensable temporal bridge.

Virtual Power Plants: Coordination at Scale

The most consequential development in Australia's storage landscape is not a single large-scale project. It is the emergence of virtual power plants (VPPs) — and what they represent architecturally.

A VPP aggregates thousands of distributed assets: residential batteries, rooftop solar systems, and EV charging infrastructure, unified through software orchestration into a single, dispatchable energy entity. No physical centralization required. Only real-time coordination.

Australia has emerged as one of the world's most active VPP testing environments. Programs led by Tesla, AGL, and Origin Energy have demonstrated that aggregated residential batteries can deliver frequency control, peak shaving, and energy arbitrage at grid-relevant scale. In South Australia — a state that has often led Australia's energy transition — VPP deployments have directly offset reliance on fast-start gas peakers during high-demand windows.

The AEMO has formalized this trajectory. In its Integrated System Plan, distributed energy resources (DER) and storage coordination are explicitly identified as essential infrastructure for maintaining grid reliability as coal-fired generation continues its retirement. That language reflects a structural reclassification: distributed batteries are now system assets, not just household equipment.

For ESS manufacturers and integrators, this means the addressable market is no longer defined solely by behind-the-meter economics. The product increasingly needs to serve two masters — the end user and the grid.

FCAS and the Economics of Speed

One of the clearest expressions of storage's new grid role is its growing participation in Frequency Control Ancillary Services (FCAS) markets.

In a renewable-heavy system, frequency deviations occur faster and more unpredictably than in coal-dominated grids. Maintaining frequency within safe operational bands requires assets that can respond in milliseconds — not the minutes that gas turbines or hydro units typically require.

Battery storage is electrochemically suited for this function. It responds near-instantaneously to dispatch signals, making it structurally differentiated from every other generation type.

AEMO's Quarterly Energy Dynamics reporting confirms that battery dispatch is increasingly concentrated in evening peak windows and system instability events — exactly the conditions where speed and precision matter most. As coal retires and solar penetration deepens, these windows will widen and multiply.

The economic implication is direct: storage is increasingly valued as a response asset, not just an energy reservoir. Megawatt-hours remain important, but dispatch capability, response latency, and integration depth with ancillary services markets are becoming the metrics that define commercial value.

This reframes how storage investments should be evaluated — and how ESS platforms should be designed.

Software-Defined Infrastructure: The New Competitive Frontier

The industry's evolving role is forcing a parallel evolution in how ESS products are built and assessed.

Earlier product generations were judged on hardware fundamentals: capacity, cycle life, round-trip efficiency, cost per kilowatt-hour. These remain necessary specifications. But they are no longer sufficient for competitive differentiation.

The value boundary has moved up the stack.

Today's leading ESS platforms are evaluated on their system intelligence: the ability to participate in VPP networks, respond to dynamic pricing signals, execute predictive load optimization, and interoperate with external grid service platforms — all autonomously, in real time.

A battery that cannot process market signals or respond to aggregation commands is economically constrained regardless of its physical specifications. Conversely, a smaller system with deep software integration can outperform a larger standalone asset in grid services revenue and system contribution.

This dynamic is particularly pronounced in Australia, where high solar saturation in distributed networks demands continuous, intelligent balancing between local generation and grid conditions. In such environments, system intelligence is not a premium feature. It is baseline infrastructure.

The practical implication for the industry: ESS is evolving from energy storage equipment to energy coordination infrastructure. The hardware houses the energy. The software determines its value.

Australia as the Reference Grid

Australia is not a unique outlier — but it is an unusually clear early signal.

High rooftop solar penetration, rapid electrification, accelerated coal retirement, and transmission bottlenecks are converging here faster than in most developed markets. These conditions expose the limitations of legacy grid design — and the potential of storage-led coordination — at a pace other markets have yet to experience.

What Australia demonstrates is a grid architecture actively mid-transition: moving from centralized generation dispatch to distributed flexibility coordination, where the primary resource being managed is not generation capacity but temporal adaptability.

In that architecture, batteries are not supplementary. They are structural. And the systems best positioned to lead — technically, commercially, and architecturally — are those designed for grid participation from the outset, not retrofitted for it.

The question for the global ESS industry is no longer whether this transition will happen. Australia has already answered that. The question is how quickly other markets will reach the same inflection point — and whether the products entering those markets will be ready.